You’ve probably seen the shows on HGTV, right? Chip and Joanna find a dingy house and make it great for a buyer, and they make themselves a nice profit doing it. Documenting the process of house flipping makes for great TV, but the most important thing for a fix-and-flip investor to get right is in the numbers and analysis. You’ve got to do a good job of estimating expenses and the after-rehab value (ARV) of a property before you buy or you may find yourself losing money when you sell!

The process that I use to evaluate a potential deal is extensive and deliberate, and I’ve built a Microsoft excel spreadsheet to help make the process run faster. My typical analysis pipeline looks like this:

1. Find a deal, either on the open market or from a wholesaler.

2. Initial deal vetting

This is where I do some back of the napkin math using my knowledge of local property values and a rough estimate of rehab costs to determine if the deal merits further analysis. This usually only takes a minute or two. I can quickly eliminate bad deals this way so I don’t waste hours of my time analyzing a deal that will never work.

3. Initial due diligence

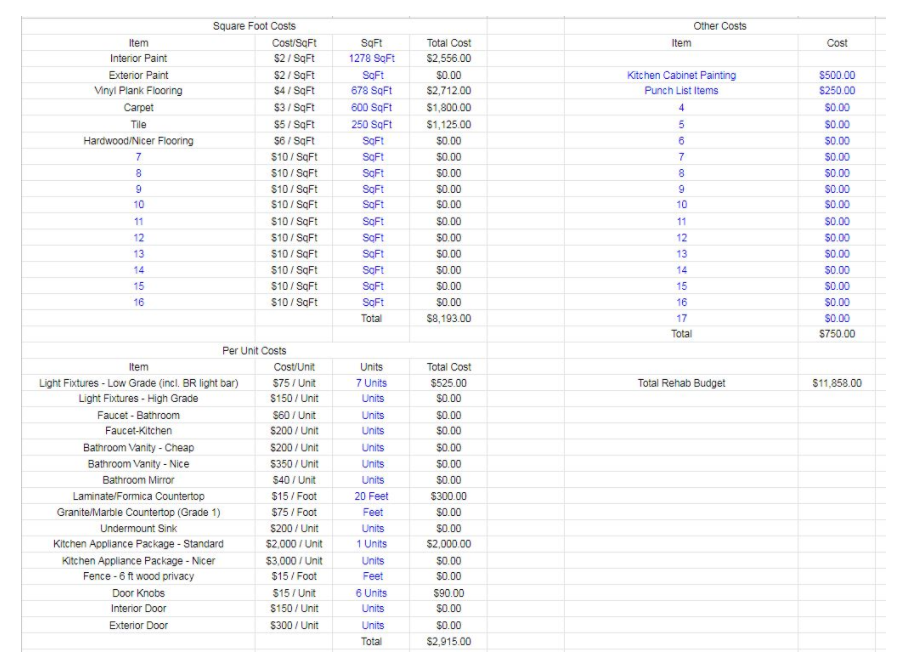

During this step I’ll conduct a more detailed analysis of comparable properties to get a more solid ARV. I’ll look at pictures of the property to narrow down a rehab budget estimate, and I’ll come up with line-item estimates of certain costs (e.g. closing costs, taxes, insurance, financing costs, utility and other holding costs, etc). I’ll plug these numbers into my spreadsheet, and if the sheet outputs a ROI over 20% I’ll do some more digging.

4. View the property

Now is the time to really nail down that rehab budget. I’ll tour the property and come up with line-item estimates of all the work required and determine how long the project will take. I’ll also be able to visualize the layout of the house when it’s renovated, which will allow me to have more clarity on my ARV estimate. I’ll plug updated numbers into my spreadsheet and then…

5. Write a contract

Do I offer to pay asking price, or do I negotiate down lower? That depends on the numbers. I have no problem paying the seller asking price if that price gives me a great ROI and will still allow me to at least break even if the ARV is 15% below my estimate and the rehab budget was underestimated. Otherwise, I’ll negotiate the price down or walk away from the deal. Remember: in real estate, you make your money when you buy.

6. Get under contract, complete due diligence, and secure financing.

I won’t talk about this too much in this post — stand by for follow up posts on these topics!

IN THE WEEDS

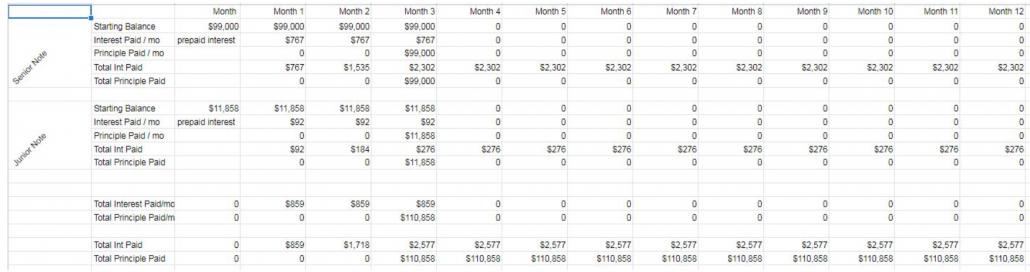

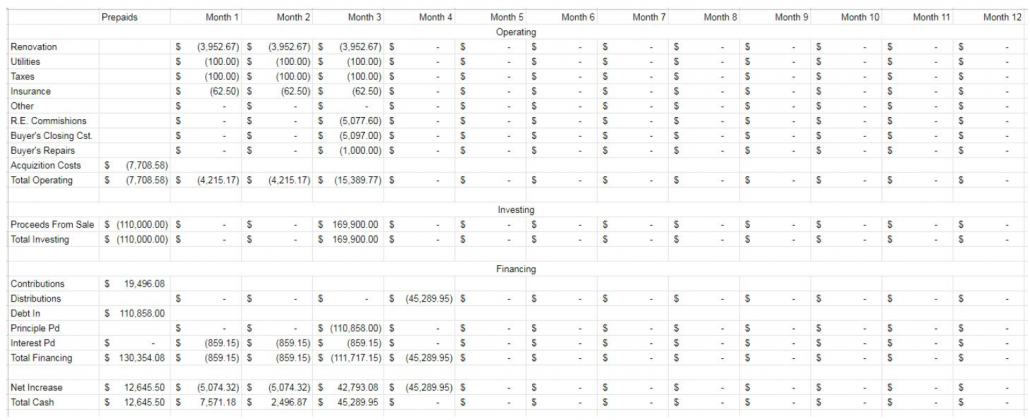

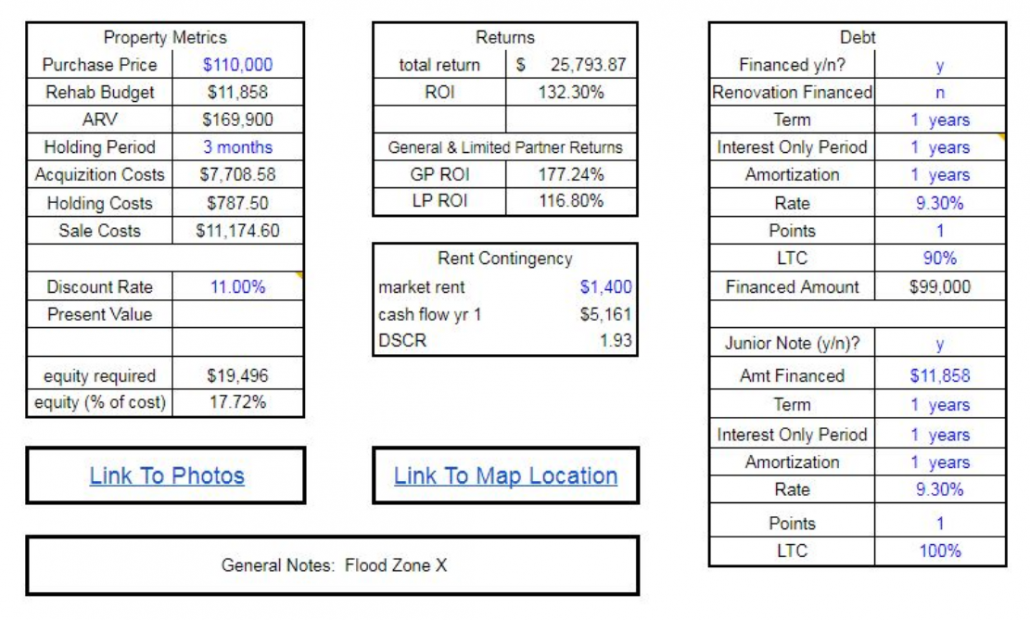

Let’s get into the details now. I’m going to include a screenshot of each individual sheet in my analysis model to show you what I’m looking for when I analyze fix-and-flip deals. I’ve set this sheet up to be a stand alone product that I can send to lenders and equity partners. Some folks use an uglier spreadsheet and put the pertinent information on a well-formatted PowerPoint presentation. Either method is fine, but I find that this way just takes less time, and time is money!