Have you ever seen The Big Short? If not, stop what you’re doing and go watch it.

If you have, you know the part where Steve Carell’s character, Mark, walks out of a mortgage lending convention and calls up his trading team back in New York to tell them to start buying credit default swaps. He & his team end up buying $500M of credit default swaps after Mark solidifies his fears that banks were mass-buying risky loans with little to no true oversight or regulation. Essentially, he knew the risky loans were going to ruin the entire market before anyone else was really even aware, and therefore decided to bet against those loans for pennies on the dollar so he could get a huge payout after the crash. (https://www.youtube.com/watch?v=ECmh0M-aHPg)

The thing is, everyone always wants history to repeat itself, and humans are naturally predisposed to see patterns in everything. Sometimes that pattern-seeking behavior helps us, sometimes not so much. In the case of the housing market in 2021, a lot of folks want to think, “Housing prices are high. Last time housing prices were high, there was a big crash. Therefore, there’s a big crash coming.” If we look deeper into the causes of the 2007-2008 great financial crisis (GFC), we will see that this market is very different.

So, what blew up the housing market back then? In short: bad loans, bad lending practices, and too much development. The bad loans were adjustable rate mortgages, and the bad lending practices were that basically anyone with a pulse could get a loan back then. This worked well for a lot of people, until it didn’t. And when it didn’t work anymore, the ensuing collapse of the housing market and mass default of mortgages almost brought down the entire world’s financial system with it.

What is an adjustable rate mortgage and why is it bad?

An adjustable rate mortgage (ARM) is exactly what it sounds like: a mortgage where the rate can adjust. Most mortgages that people take out are at a fixed rate over a thirty year term, but some people take out ARMs. An ARM typically has a lower interest rate for the first 1-5 years, then, for the remainder of the term, the rate will typically increase and fluctuate based on some benchmark rate, like the ten-year US treasury. As the benchmark rate goes up or down, so does the rate of the mortgage.

An ARM can sometimes be a good thing to get, like when you are pretty certain you’ll end up selling the home before your low teaser rate expires (and hopefully end up selling for more, as is typically the case because the U.S. housing market over the last 80 years has gotten more expensive almost every year).

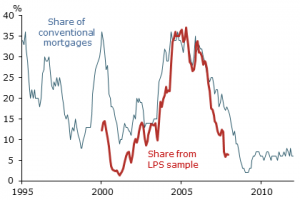

A lot of people were doing this in the mid-2000s as the housing market skyrocketed. They would get a loan on a low-rate ARM, thinking they would sell in a year or two for a handsome profit.

As a result, ARM products became very popular in the 2000s and many of the loans saw their low teaser rate expire in 2006-2008 – just as the wider economy was slowing down and the housing market was beginning to collapse.

Source: LPS Applied Analytics and Freddie Mac, https://www.frbsf.org/economic-research/publications/economic-letter/2012/november/housing-boom-mortgage-choices/

This was obviously pretty bad timing for a large number of folks who were betting on being able to get out of their ARMs before the teaser rate expired. Folks who intended to sell were not able to do so, and folks who intended to refinance into 30 year fixed rate mortgages were also unable to do so as their houses were unable to appraise as they became less valuable. Many folks were unable to come up with enough money to pay the higher rates and simply walked away from their homes.

What about bad lending practices?

The widespread use of ARMs does not fully account for the problem. ARMs in and of themselves are not bad; a well-qualified buyer should be able to cover the higher payment that results from the expiration of the teaser rate. The problem in the mid-2000s is that many of these buyers were simply not qualified to purchase a house.

If you’ve bought a house since the GFC, you probably know what a pain in the ass it is to get a mortgage. Your lender would have asked you for bank statements, tax returns, may have asked you to explain large transactions in your bank accounts, etc. They do all of this to make sure that you are actually capable of making payments on the loan that they are going to give you. This is a good thing!

Back then, many banks simply were not doing this. Buyers were getting loans without being made to prove any of the income or asset declarations they made on their loan applications. The practice became so prevalent that it even got the name, the NINJA loan: No Income, No Job, No Assets. This wasn’t a problem during the teaser rate period of an ARM mortgage, but as soon as the rate increased many of these borrowers immediately defaulted on their payments.

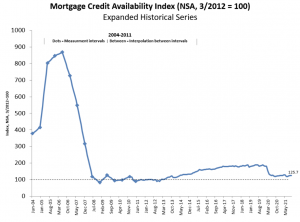

The Mortgage Bankers Association (MBA) puts together a system of tracking how easily buyers can get credit to purchase homes, which is called the Mortgage Credit Availability Index (MCAI). In October of 2006, this index hit a peak of about 900. (The index currently sits at 125.)

https://www.mba.org/news-research-and-resources/research-and-economics/single-family-research/mortgage-credit-availability-index

How could they afford to do this?

You may be thinking to yourself, “Wouldn’t it be prudent for the banks to make sure that their borrowers can repay the loans?” Yes, it would be – if the bank intended to keep the loan on their books. But they sold these loans to other, larger institutions like pension funds, investment banks, & Fannie Mae & Freddie Mac. So once these loans were off the bank’s books, there was no more risk (for the bank). These big players were not diligently inspecting the loans that they were buying. There is a LOT more to it than this – for more detail, you can always watch Margot Robbie explain it.

So what does all this mean?

You don’t have to be an economist to know that the price of any item in any market is driven by supply and demand. Lending practices in the mid-2000s caused a massive increase in demand as millions of buyers who would not normally have been able to buy a home suddenly entered the market.

So far, we’ve touched on the demand side of the equation. Let’s take a look at supply. The chart below shows single family homes that are permitted for construction going back to 1960.

You can see that there’s lots of natural variability, but that, for the most part, the average is about 1,000,000 units started each month, and almost never more than 1,400,000 until about 2002. Houses started then began to rise all the way to a peak of 1,800,000 in 2006, before falling off a cliff at the start of the financial crisis before most economists even knew what was happening.

Builders were building more homes to meet demand for new homes, naturally. But much of this demand was artificial demand fueled by these bad lending practices. When the music stopped and the bottom fell out, suddenly there were too many damn houses! Check out that graph after the recession officially ended in late 2009 – it took ten whole years for housing starts to crawl back up to the long term average of 1,000,000!

Why is today different?

First, almost nobody is getting ARMs. Why would you, when you can get a 30 year fixed at 3%? Not much else to say there; the ARM is essentially dead for the time being.

Second, mortgage bankers are properly underwriting loans. Remember that Mortgage Credit Availability Index we talked about earlier? Go take another quick look at that. Don’t believe me? Apply for a loan yourself and see how many documents your lender makes you turn in! By and large, only qualified borrowers are getting loans, and they’re getting them at fixed rates, meaning their payments won’t increase.

Third, supply. Remember the housing starts chart a few paragraphs ago? Take another look – the oversupply of homes that we had in 2006 has all been consumed by the market and then some. We now have an undersupply of new homes. So many builders went bankrupt in 2006 that it really has taken the better part of a decade for that industry to recover, and in that time, the millennial generation has started to enter their prime home buying years.

The chart below shows what’s known as “months of inventory”.

In a balanced housing market, there should be about six months of inventory on the market. Currently, across the entire US Housing market, there are just over 6 months of inventory – this number was below 4 months at the peak of the COVID-related supply crunch.

In the Savannah market specifically, months of inventory is around 2 months at the moment. Savannah is still very much suffering from lack of inventory, and local price increases over the last 2 years have been driven largely by this lack of supply.

What does all this lead me to believe?

- Increases in housing prices have not been driven by bad lending, and are more likely a result of a lack of supply.

- As supply catches up with demand, it is likely that the rate of growth in housing prices will slow down to more typical historic levels of about 3% price growth per year nationally.

- I believe that Savannah in particular will see higher than average price growth due largely to the fact that Savannah has been and will continue to experience more population growth than the larger United States. For more information on this, check out another blog here.

Actions speak louder than words though, so here’s what actions I’ve been taking: I’ve more than doubled my personal Savannah area real estate holdings in 2021. Could I be wrong about all of this? Maybe – but I have enough conviction in my beliefs that I’m willing to bet a substantial amount of money that I’m right.

—

Written by: Pat Wilver